From the People and Nature blog.

The UK government claims, extravagantly, that it is aiming for “net zero”. But the devil is in the detail. Here, PETER SOMERVILLE goes through the government’s Net Zero Strategy with a fine-toothed comb – and shows how its promises are exaggerated and its numbers don’t add up. It falls to pieces in your hands

When government ministers published their Ten Point Plan a year ago, they recognised that it did not go far enough to fulfil their international commitment to reducing carbon emissions. One year on, their Net Zero Strategy (NZS) goes a little further, but still falls far short of what is required. The problems inherent in the original plan persist, namely:

- A failure to recognise that the world is now experiencing a climate emergency, and therefore that more drastic action is required in the short term (before 2025) to reduce carbon emissions. The reductions up to 2025 are minimal (page 18, Fig 1, or p. 77, Fig 13. Note: all page numbers in this article refer to the Net Zero Strategy, unless stated otherwise.)

- A continuing (and increasing) reliance on problematic technologies that do not currently exist at scale, particularly carbon capture, use and storage (CCUS), and direct air carbon capture.

- A failure to explain clearly how expected future carbon savings have been calculated, particularly in industry, buildings and transport.

- A neglect of issues relating to agriculture, food, land use and energy storage.

- An emphasis on constructing new nuclear power plants, with a new (from 2022) Future Nuclear Enabling Fund of £120 million, but – as the UK FIRES commentary on the government’s plan shows – with no net increase in nuclear power capacity likely until after 2030. In the meantime, construction work adds significantly to carbon emissions.

- An emphasis on GDP growth, despite the strong correlation between such growth and increasing carbon emissions.

- A lack of clarity about how specific policies could achieve intended emission reductions, e.g. on hydrogen.

- A failure to curb the expansion of aviation to 2030 and beyond (an expansion that is encouraged rather than hindered by the latest spending review’s decision to cut air passenger duty).

- A failure to take account of other government programmes that increase rather than reduce emissions, e.g. increased spending on roads (£27 billion) and defence (£24 billion) up to 2024.

The government has already committed to invest £25.5 billion for a Green Industrial Revolution (£12 billion under the Ten Point Plan, £9.7 billion for 18 deals at the Global Investment Summit in October 2021, and £5.8 billion on other sustainable projects since the Ten Point Plan). Together with £40 billion for the new UK Infrastructure Bank (p. 206), and leveraging £90 billion of private investment, this funding is expected to support 440,000 jobs in 2030 (pp. 16, 17 and 49).

The NZS describes three future scenarios, but arguably only Scenario 1 (high electrification) is really worth considering.

□ Even Scenario 1 has serious limitations. For example, as with the other scenarios, it takes no direct account of uncertainty about future technology costs and availability (p. 316). So much for the precautionary principle, one might argue.

□ Scenario 2 is based on a hydrogen-dominated pathway, even though the NZS is already committed to electricity as the main source of so-called “low-carbon” domestic heating. (It seems to be assumed that electricity generation will be fully decarbonised by 2035).

□ And Scenario 3 (high innovation) is based largely on wishful thinking about green aviation and direct air capture.

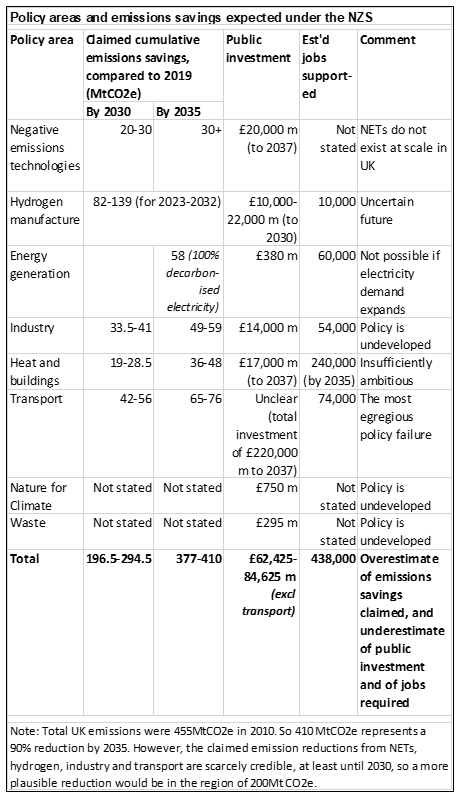

The Table sums up the proposals in the NZS.

Negative emissions technologies

The discussion of negative emissions technologies (NETs) in the Strategy is difficult to follow. It talks about carbon capture of 20-30 million tonnes of carbon dioxide (MtCO2) per year being required to meet the increase in electricity demand (primarily for electric vehicles and heat pumps) by the early 2030s (p. 82 and p. 126), and at least 50 MtCO2 by the mid-2030s.

Some of this is for industry – 9 MtCO2 a year by 2035 is mentioned (p. 88 and p. 120) – and some for direct air capture, but the details are unclear. Some must be for “blue” hydrogen manufacture, but this is not specifically mentioned.

The Technical Annex provides figures of 7 million tonnes of carbon dioxide equivalent (MtCO2e) per year by 2035 of industrial CCUS, and 23 MtCO2e per year by 2035 of bioenergy carbon capture and storage (BECCS) and Direct Air Carbon Capture and Storage (DACCS) (Table 10, pp. 325-6, see also p. 89 and p. 188). So the total envisaged removal may well be 30 MtCO2e per year by 2035, at least under the preferred high electrification scenario. (Confused about MtCO2 and MtCO2e? The NZT seems to be. See Note at the end of this article.)

As the Strategy says (p. 82), this is certainly more than double the level of NETs than was stated in the Ten Point Plan. It is in fact three times as much. And it rises to 75-81 MtCO2e a year by 2050 (p. 189 and p. 318, Table 4).

Overall, therefore, this is a much bigger carbon unicorn than a year ago, but that does not mean it has become any less unreal. Three times a fantasy is just a bigger fantasy.

For useful summaries of the benefits and problems of using biofuels, see The Biofuel Controversy and Economics of Biofuels. On BECCS, see Can BECCS help us get to net zero? To which the answer is: at best, only slightly … and that is assuming that the biofuel is sustainably sourced, which is usually not the case.

A total of £20 billion of public and private investment is said to be required for greenhouse gas removals up to 2037 (p. 192), which seems a considerable sum to risk on technologies that will not be viable at scale in the UK before 2030.

Electricity

The Strategy commits to £380 million for offshore wind by 2035 (p. 94), which is more than twice the £160 million pledged in the Ten Point Plan, with a budget of £200 million already allocated to fund Contracts for Difference (a pricing mechanism that fixes the wholesale purchase price of renewable electricity). However, the Ten Point Plan’s offshore wind targets of 40GW (quadrupling current capacity) and 60,000 jobs by 2030 remain.

Onshore wind is now being permitted, but there is no provision for public investment or target setting either in onshore wind or solar. The relevant industry bodies estimate that by 2030 onshore wind capacity could reach 30 GW (currently 14 GW), and solar power capacity at least 28 GW (currently 14 GW), or as much as 40 GW if linked to new build and deep retrofit programmes.

In terms of electricity generated in 2030, this amounts to 128 Terawatt hours per year (TWh/year) from offshore wind (quadrupling the current output) plus about 68 TWh/year from onshore wind (more than doubling the current output) and 26 TWh/year from solar power (doubling current output). (See also this report, p. 7.)

Total electricity generated from wind and sun in 2030, therefore, on the basis of current government pledges and likely market provision, would be around 222 TWh/year, compared with the current generation of 77 TWh/year (64 TWh/year from wind, 13 TWh/year from solar). This is a major increase, but the demand for electricity is set to rise substantially due to the electrification of transport and heating systems, the need for renewable energy storage, the manufacture of “green” hydrogen, and industrial decarbonisation generally. The UK FIRES engineering research group estimates that 960 TWh/year will be required by 2030, so there remains a huge shortfall.

The Strategy (pp. 88-89) envisages a fully decarbonised electricity network by 2035, but this seems to be possible only on the basis of massive and overwhelmingly private investment (at least £280 billion) and the abatement of emissions from fossil-fuel power stations (i.e. CCUS). No closures of gas-fired power stations are planned in the current decade.

Carbon emissions from this sector are expected to be reduced from 58 MtCO2e in 2019 by 80-85% by 2030, that is, to 9-12 MtCO2e (pp. 95-6). This is a reduction of more than 46 MtCO2e – more than twice the 21 MtCO2e reduction, due to offshore wind alone, from 2023-2032 pledged by the Ten Point Plan.

Presumably, much of this will be achieved by deployment of onshore wind and solar, but this is not stated in the Strategy. So it is not clear here how much the Strategy is relying on CCUS and other NETs, which will not be available at scale in the UK until after 2030.

The private investment could be forthcoming, as the national grid is driving electricity decarbonisation, but this is not discussed in the Strategy. The issue of energy storage, to allow for the intermittency of wind and solar energy, is also not addressed – though there is a reference to the possibility of using hydrogen for this purpose (p. 98).

Given the uncertainties associated with CCUS, as with NETs more generally, it would make more sense to aim for higher capacity for renewable electricity generation, relying not only on offshore wind but also onshore wind and solar energy. It would make sense, too, to give more serious attention to how this energy is to be stored so that it is available in sufficient amounts when the sun doesn’t shine and the wind doesn’t blow.

However, it seems unlikely, to say the least, that this will be sufficient to meet the expected future demand for electricity, so fossil fuel use will continue … unless demand is substantially reduced. Meanwhile the government continues to support oil and gas and has not ruled out opening new coal mines, not to mention the scandalous case of Drax. This all serves to reinforce the conclusion that the Strategy’s expected emissions reductions in this area of policy are just not credible.

Hydrogen

The Strategy repeats the commitment, made in the Ten Point Plan, to build 5 Gigawatts (GW) of “low-carbon” hydrogen manufacturing capacity by 2030, claiming to achieve emissions savings of 41 MtCO2e from 2023 to 2032, and adds an aim to provide 10-17 GW by 2035 (depending on whether the pathway follows Scenario 1 or Scenario 2) (pp. 109-110), which at this rate would save 82-139 MtCO2e. The Strategy envisages a mix of “green” hydrogen (produced by the electrolysis of water) and “blue” hydrogen (produced mainly by the steam reforming of natural gas (methane)) (p. 110). It does not state what the nature of this mix might be or how it might change through time.

The construction of hydrogen capacity is supported initially by a Net Zero Hydrogen Fund of £240 million (p. 121), with an expected additional total investment of £10-22 billion up to 2030 (for Scenarios 1 and 2, respectively) (p. 110). This seems to constitute an additional commitment compared to the Ten Point Plan, e.g. supporting 10,000 jobs rather than 8,000 jobs, but it is not clear how much of this additional investment is expected to be public (£500 million was pledged in the Ten Point Plan).

Under Industrial Decarbonisation and Hydrogen Revenue Support, the Strategy offers £100 million for projects to make “green” hydrogen (p. 127). But it also seems to assume (incorrectly) that the production of “blue” hydrogen is “low carbon”.

The use of “blue” hydrogen is problematic for two reasons:

□ First, rather than moving away from fossil fuels, it depends on their continued use (specifically of natural gas); and

□ Second, it depends on the application of carbon capture and use technologies that do not yet exist at scale in the UK. (See Negative Emissions Technologies, above.) One might imagine that the claimed emissions savings are based on a comparison with the manufacture of hydrogen from natural gas without CCUS (“grey” hydrogen), but this is not mentioned in the Strategy.

“Green” hydrogen is to be preferred, as it marks a step away from using fossil fuels, but it is also a technology that does not yet exist at scale in the UK. It offers potential, because 5 GW of electrolysers could produce around 28-33 TWh a year of hydrogen energy, which seems to compare favourably with offshore wind (10 GW generating 32 TWh a year). It is also true that hydrogen can be produced relatively efficiently by electrolysis.

However, there are two drawbacks: first, the electricity being used to make “green” hydrogen is not generated entirely from renewable sources, and will not be until the national grid is fully decarbonised (possibly by 2035); and second, the energy return on energy invested (EROI) for “green” hydrogen (0.8-0.7) is far lower than the figure of 18 for offshore wind as stated here.

The talk about “efficiency” obscures the fact that it takes more energy to produce hydrogen than the energy supplied by that hydrogen. Of course, energy is required to manufacture wind turbines and solar panels, to maintain them, to connect them to the grid, and so on, but the wind and sun are freely available – whereas the electricity that powers the electrolysers is itself generated by those turbines and panels (and by fossil fuels) and comes at a cost.

Whereas the generation of electricity directly from renewable energy replaces fossil-fuel generated electricity on the national grid (that is, unless total electricity supply demand increases), the generation of “green” hydrogen represents a loss of electricity to the grid.

It is difficult to see, then, how “green” hydrogen manufacture can reduce emissions at all, although it could still be important, for example, for storing energy or for powering large vehicles that cannot be moved by electrical means.

Industry

The Strategy’s discussion of industrial emissions is complicated by its – arguably misplaced – reliance on CCUS. It envisages emissions reductions from CCUS alone of 6 MtCO2 a year up to 2030, and 9 MtCO2 a year by 2035, funded largely by a £315 million Industrial Energy Transformation Fund, which will be extended to £500 million to 2028 in order to fund industrial retrofits, to achieve net zero industrial clusters (pp. 120-121 and 131).

In addition, resource efficiency and energy efficiency measures are expected to achieve 11 MtCO2e savings by 2035 and a further 9 MtCO2e by 2050, and the Industrial Decarbonisation Strategy published in March 2021 has allocated an additional £171 million for nine projects in five clusters. But the UK FIRES team states (p. 10) that this strategy is unlikely to produce emissions savings.

Perhaps more importantly, the new UK Emissions Trading Scheme cap will be aligned with the net zero trajectory by 2023, which is expected to result in a reduction in industrial emissions from a total of 78 MtCO2e in 2019 by 43-53% (33.5-41 MtCO2e) by 2030, and 63-76% (49-59 MtCO2e) by 2035 (p. 121).

Such large possible reductions were not mentioned in the Ten Point Plan but, as with hydrogen and CCUS, detail is missing on how this level of reductions could be achieved. Mention is made of “fuel switching” (£55 million for a switching competition and £40 million for a Red Diesel Replacement competition (p. 126 and p. 129)), energy efficiency, CCUS, carbon pricing, and demand-side measures such as product labelling, regulatory standards, and changes to procurement approaches. Total additional investment of £14 billion is expected, supporting 54,000 jobs in 2030 (p. 124). It would be good to know more about how this money might be spent.

Possibly most important of all is electrification, which is expected to reduce emissions by 5-12 MtCO2 a year by 2050 – 5 if hydrogen is available, 12 if not (p. 128). Once again, calculating total emissions is impossible, because the Strategy does not provide year-on-year estimates from which totals can be calculated. Again, the failure to provide such estimates or totals tends to suggest that decarbonisation is still not being taken seriously enough – the UK FIRES team states baldly (p. 12) that, for the manufacturing sector, these measures “will not directly bring about any meaningful physical changes by 2030”.

Overall, the Strategy on industry looks undeveloped and not sufficiently coherent. Regulatory standards are not envisaged to come into force until the late 2020s (p. 131). In view of the climate emergency, much bolder and clearer regulation is required, e.g. to phase out fossil fuel use and to follow the three “R”s: reduce, reuse and recycle.

Heat and buildings

The policy on heat and buildings is largely unchanged since the Ten Point Plan, either in the NZS or in the separate Heat and Buildings Strategy (HBS), published at the same time. There is a target for as many buildings as possible to reach at least Energy Performance Certificate (EPC) level C by 2035, and as many fuel poor homes as reasonably practicable to reach level C by the end of 2030; and for the installation of up to 600,000 heat pumps a year by 2028.

The Strategy envisages that after 2028 heat pump installations will increase, to 1.9 million a year (1.7 million according to HBS, p. 16) by 2035 under the electrification scenario, resulting in about 13 million electrical heat installations (11 million homes with heat pumps and 2 million using heat networks) (p. 141). Under the hydrogen scenario, 4 of these 11 million would use “low-carbon” hydrogen instead – and again, it is not clear how much of this would be “green” hydrogen by 2035. The Strategy assumes that a typical heating appliance has a lifetime of 15 years, so proposes that no new fossil fuel installations should be allowed after 2035, in order to reach the 2050 zero emission target (p. 340).

The Strategy envisages that investment of £200 billion will be required up to 2037 to achieve this transformation, but does not elaborate on the balance between public and private investment. There are two clues to what this balance might involve, however, in the HBS. 1. The total cost of the government heat and building programmes from 2021 to 2025 is said to be more than £5 billion (HBS, p. 35), and this spending of around £1 billion a year is then expected to increase up to 2035. 2. The HBS sees the Energy Company Obligation (ECO) increasing from £640 million in 2022 to £1 billion in 2026, and by a further £1 billion a year up to 2030 (HBS, p. 140). So the total public investment to 2037 is likely to be more than £17 billion, and the private investment for ECO alone will be at least £9 billion. This leaves open the question of where the remaining £174 billion will come from!

The total public subsidy for heat pump installation could amount to £55 billion (grants of £5,000 each for 11 million heat pumps), and the government contribution to retrofitting buildings to EPC level C is likely to be in a similar ballpark, but has not been stated here. Reference is made to supporting more than 240,000 low-carbon jobs by 2035 (NZS, p. 135) (much higher than the 50,000 jobs pledged in the Ten Point Plan), but neither strategy explains how this figure has been reached.

Emissions from the heat and buildings sector are now around 77 MtCO2e/year. The NZS says that emissions could fall by 25-37% by 2030, and 47-62% by 2035, compared with 2019 – rather less than the 71 MtCO2e for 2023-32 cited in the Ten Point Plan (p. 139).

The only policy for which emission reductions are pledged is the Public Sector Decarbonisation Scheme for public sector buildings – 50% by 2032 and 75% by 2037 (p. 136 and p. 147). But public sector buildings are responsible for only 2% of total UK emissions.

The UK FIRES team has calculated (see here, p. 18) that a linear expansion of heat pump installation to meet the government’s 2028 target would save only 6.5 MtCO2e/year, and even this estimate probably assumes that the electricity supply is decarbonised.

Scotland has 5% of the UK’s homes, and its Heat in Buildings Strategy for these looks similar, with £1.8 billion of public investment over five years, and cashback grants to homeowners in the Home Energy Scotland Loan Scheme, of up to £6,000 for energy efficiency improvements and up to £7,500 for new renewable heating. (NZS, p. 150).

Two other points are worth noting.

□ First, the HBS (pp. 87-91) assumes that a building in EPC band C or above does not need to be retrofitted to low carbon, however “low carbon” is interpreted. This assumption is false, but we do not know what retrofitting is required for the 10 million homes that it ignores. The HBS also seems to assume that a property in EPC band D can reach band C by insulating loft and cavity walls, and “modest draught-proofing and smart controls” (p. 90). In fact, in many cases much more is required, such as insulation of floors and double or triple glazing, and other alterations – which means that retrofitting will cost significantly more than HBS considers.

□ Second, the Strategy aims to reduce the costs of electricity (and hydrogen) relative to natural gas, so that low-carbon heating appliances (mainly heat pumps but also possibly “green” hydrogen fuels in the future) will be the preferred choice. To accelerate this change, HBS favours a market-based mechanism for low-carbon heat, which involves an obligation on fossil-fuel heating appliance manufacturers to achieve sale of a certain level of heat pumps proportional to their fossil-fuel boiler sales in a given period (see this document, p. 11). This mechanism is similar to the Energy Company Obligation for power supply, and is intended to be used to phase out the sale of fossil-fuel heating systems by 2035, though it is not being considered for introduction until 2024. By the same token, however, higher and increasing proportions of heat pump installation over shorter periods could achieve more, and by an earlier date. Why not 1 million heat pumps by 2025, for example, with new gas boilers being banned from 2028 (as proposed by UK FIRES, p. 18)? This would help to ensure zero emissions from heating systems well before 2050.

As for new homes, a Future Homes Standard is pledged to come into force in 2025, resulting in 75-80% lower emissions (HBS, p. 134). It is difficult to understand, however, why this long-postponed measure should not come into force as soon as possible, e.g. by 2023, along with other reforms such as zero VAT for retrofit.

Transport

From a total of 124 MtCO2e emissions in the domestic transport sector in 2019, the Strategy talks of reductions of 34-45% (42-56 MtCO2e) by 2030, and 65-76% (81-94 MtCO2e) by 2035 (p. 154). This requires total additional investment by 2037 of £220 billion, supporting 22,000 jobs in 2024 and 74,000 in 2030 (p. 157). This compares with 40,000 jobs, for electric vehicles alone, in the Ten Point Plan. It is not clear how these figures are arrived at or how much public investment is at stake. The strategic roads programme of £27 billion public investment is not mentioned, nor the £23 billion public money committed to the HS2 rail link by 2025.

Private motor vehicles

The key policy here is the zero emission vehicle (ZEV) mandate, which from 2024 will set targets requiring a certain percentage of new car and van annual sales to be zero emission rising to 100% in 2030 (p. 160). This is expected to result in 53% of cars and 40% of vans being ZEVs by 2035, with emissions savings being somewhat less than this if the total numbers of cars and vans increase (p. 326).

Cars are currently responsible for the bulk of transport emissions – 68 MtCO2e in 2019 – so this could still mean substantial emissions savings by the early 2040s (p. 153). However, the exact amount of savings is unclear – and is likely to be far less than the Strategy claims, for three reasons:

First, it seems to be assumed that electric or hydrogen-fuelled vehicles are zero emissions but this is not the case.

Second, the extent of emissions reduction depends on how quickly the electricity grid is decarbonised. Obviously, the quicker the better, so that the ZEV mandate can be front-loaded – that is, come into force earlier, e.g. by the end of 2022, and involve higher percentage reductions by an earlier end date, say, 2026, resulting in zero tailpipe emissions well before 2040. This front-loading looks unlikely, however, since the charging infrastructure for electric vehicles (EVs) remains undeveloped, and the Strategy promises only an EV infrastructure strategy later in 2021 (p. 152). A sense of urgency is still lacking.

Third, it has been estimated that any emissions savings made by the transition to EVs will be largely negated by the government’s £27 billion investment in roads. The Strategy is generally encouraging rather than discouraging car use, and offers very little to reduce the impact of cars on the environment, e.g. by ensuring that they are constructed from lighter weight materials and designed to have lower impact.

Given all these problems, it makes no sense for the Strategy to offer £620 million for EV grants, plus a further £350 million from the Automotive Transformation Fund to support vehicle electrification – particularly since EVs are cheaper to run and incur no fuel duty … which continues to be frozen at 2011 levels, providing a huge boost to fossil fuel consumption.

For vehicles that continue to need liquid fuel, the Renewable Transport Fuel Obligation (RTFO) will increase the proportion of renewable fuel required in the mix from 9.6% in 2021 to 14.6% in 2032, and extend this obligation to the maritime sector. This means that the RTFO could result in additional emissions savings of 21 MtCO2e (pp. 161-3) – but this would depend on the nature of the renewable fuel, which is not specified (e.g. “blue” hydrogen could be included).

Overall, it is clear that the whole area of the Strategy’s policy on cars is incapable of delivering the emissions savings that it expects.

Trains, buses, cycling and walking

Policy here is largely unchanged from the Ten Point Plan – that is, £3 billion for 4,000 zero emission buses in the National Bus Strategy, which should reduce bus emissions by about 0.4 MtCO2 by 2030, and £2 billion for cycling and walking (segregated cycle lanes and low-traffic neighbourhoods), though this is now by 2030 instead of by 2025 (pp. 152-3). Some of this has clearly been spent already, but the Strategy does not say how much.

Most interesting, perhaps, is the £12 billion allocated for local transport systems up to 2024, based on Local Transport Plans, a significant increase on the £4.2 billion pledged in the Ten Point Plan (p. 152 and p. 163). Most disappointing is the lack of support for rail decarbonisation, with the rail network expected to be net zero only by 2050 (p. 153 and p. 156).

The Scottish government is committed to decarbonise rail by 2035, provide £500 million for bus infrastructure, £500 million for active travel projects over five years, and free bus travel for under-22 year olds (p. 165). Comparable funding in England would mean £10 billion for buses and £10 billion for cycling and walking – a considerable improvement.

On the UK level, as in the Ten Point Plan, it is unclear how much the government will invest in improving and renewing the rail network.

The UK lags far behind other developed countries in this respect, and its rail network could well be fully electrified by 2030 or earlier. Perhaps worst of all is the Strategy’s failure to identify measures that can be clearly seen to produce the modal shift from private to public transport that it says it wants to achieve.

Aviation

The emphasis here is on developing Sustainable Aviation Fuel (SAF), so as to provide 10% of total aviation fuel by 2030, with state support of £180 million (p. 153 and p. 162). This is pie in the sky, for two reasons.

First, as aviation is being allowed to expand by more than 10% up to 2030, it means that carbon emissions will increase over this decade, when they are supposed to be reduced.

Second, the use of SAF has been touted for decades with no real progress at all: whether in the form of biofuels or e-fuels, SAF will do nothing to reduce the warming effect of contrails, which is estimated to be three times as great as that of carbon dioxide emissions.

The argument against SAF holds even without mentioning the strictly limited availability of biomass for biofuel and the high costs of producing e-fuel.

Under the government’s electrification scenario, international aviation and shipping has by far the highest level of emissions in 2050 – 35 MtCO2e – requiring the lion’s share of greenhouse gas removals (p. 318, Table 4). This is even without taking into consideration the problem of contrails.

All things considered, tackling climate change requires an end to airport expansion, fair taxation of aviation fuel (currently exempt) and other measures to ensure that aviation pays its fair share of what is needed to achieve a safer world.

Natural resources

There appear to be two kinds of activity here: first, to enhance carbon sinks such as peatland and woodland; and second, to make the farming and food industry more sustainable.

Carbon sinks

The key fund for carbon sinks is the Nature for Climate Fund: £750 million to be spent by 2025 on restoring peat and creating and managing woodland (p. 167). The main item is £500 million for planting 30,000 hectares of trees a year, which will be continued from 2025 onwards, and the rest is for restoring 35,000 hectares of peatland in England (pp. 165-7). By 2050, the strategy expects that 280,000 hectares of peatland will be restored, with the help of funding under the new Environmental Land Management Schemes being put in place after Brexit (p. 178).

The peatland restoration plan could be more ambitious, particularly as peatland continues to be degraded, and the Strategy contains no estimates of the amount of carbon that is likely to be sequestered by these programmes.

The England Peat Action Plan aims to end the horticultural use of peat in the amateur sector by 2024 and to consult on potential legislation, e.g. to ban peat sales altogether (p. 177). But why waste time consulting, when ending the extraction and sale of peat is clearly the right thing to do?

The Scottish government plans for 250,000 hectares of peatland to be restored by 2030, and 18,000 hectares of new woodland created each year up to 2024-25, with the latter being supported by a fund of £150 million (p. 180). These plans are on a different scale from those in England.

The Strategy says: “We have rewetted around 100,000 hectares of peatland across the UK” (p. 169). This is a real achievement, but most of it has probably been in Scotland, where two-thirds of UK peatland is found.

Farming and food

It is good to see that things have moved on since the Ten Point Plan, when this topic was barely mentioned. From 2022, a Farming Investment Fund will offer financial incentives to improve animal health and welfare and reduce emissions from animals, and provide grants for equipment, technology and infrastructure, to reduce slurry pollution and methane emissions, and protect and restore biodiversity (p. 176). However, the Strategy does not provide details of this fund.

Three new environmental land management schemes will then come onstream in 2025, to incentivise farmers to adopt low carbon practices (e.g. soil and nutrient management), to support local nature recovery and deliver local environmental priorities, and to fund long-term land use projects such as peatland restoration and large-scale tree planting as mentioned above. Again, however, it is not made clear how much funding is likely to be available under these schemes.

Overall, the Strategy seems insufficiently ambitious, with farmers needing only to be “engaged with low carbon practices” (p. 171). This seems to rule out regulation. But what is to be done about farmers who do not engage? Local authorities, in contrast, are to receive £295 million to pay for free separate food waste collections for all households from 2025, to end biodegradable waste to landfill (p. 168 and p. 179).

Other provisions on waste under the Environment Bill will require local authorities to collect separately certain materials for recycling: paper and card, glass, metal, plastic, food waste, and household garden waste (pp. 179-180). A new deposit return scheme for drinks containers, and extended producer responsibility for packaging disposal, will place the net costs of disposal on producers. And in 2022 a plastic packaging tax will be introduced, at £200 per tonne, payable by manufacturers and importers of plastic packaging that contains less than 30% recycled plastic.

This is all worthwhile, of course, but the Strategy contains no assessment of what it might mean in terms of environmental amenity, consumer benefit or emissions reduction.

The urgent need to transform farming away from industrialised energy-intensive systems and towards an agro-ecological approach, and the need to reduce our reliance on livestock and move towards more plant-based diets, are not mentioned. These are serious omissions. The result is a Strategy in which the agriculture, forestry and land use sector continues to emit 14-21 MtCO2e/year in 2050 (p. 318, Table 4) – when it should be acting as a carbon sink.

International collaboration

The Strategy repeats the May government’s pledge in 2019 to double International Climate Finance from £5.8 billion in 2016-21, to £11.6 billion from 2021-25, e.g. to protect and restore nature, to access technical expertise to limit emissions and build back greener (p. 284).

The government is calling for: an immediate global end to new unabated coal power and international coal financing; a halt to natural forest loss by 2030 – now agreed by over 100 countries at COP26 – and the restoration of millions of hectares of degraded landscapes and forestlands; to accelerate the shift to ZEVs by 2035 for all new car sales (p. 288); and for developed countries to mobilise $100 billion a year in climate finance for developing countries up to 2025, as agreed originally in 2009 but never actually implemented.

Further, the Strategy mentions Boris Johnson’s pledge at the Climate Ambition Summit in 2020 to end direct government support for new fossil fuel energy projects overseas (p. 289), although massive funding continues for existing projects, e.g. in Mozambique. The Strategy also promises a new 2030 Strategic Framework in 2022, with a common vision on climate and biodiversity, and clear priorities for UK international climate and nature action to 2030 (p. 297).

Overall, then, some positive rhetoric but little detail on concrete actions that could be taken now and in the near future. The UK government is not joining the new Beyond Oil and Gas Alliance (though Wales has joined) and the UK continues to be one of the five worst fossil fuel offenders. Moreover, the government’s rhetoric has to be viewed against their cut in the overseas aid budget from 0.7% to 0.5% of GDP and a history of climate finance being mainly in the form of loans rather than grants, thus helping creditors (largely in the global North) more than debtors (mainly in the global South).

Overall investment and savings

The Strategy gives estimates for additional annual investment requirements under the NZS pathway (p. 328, Table 11). Total investment figures are not provided, but I have calculated that these amount to £675-783 billion up to 2037. This can be compared with the estimate of additional resource savings from reduced use of oil and gas products of £180 billion, over about the same period (p. 49). As elsewhere in the Strategy, the balance between private and public investment or savings is not stated.

Nevertheless, it seems clear that the level of both private and public investment required is far greater than the expected savings.

Conclusion

In spite of progress in a number of areas, for example on the decarbonisation of electricity and industry, and possibly on restoring peatland, planting trees and reducing waste, this Strategy is little changed from the Ten Point Plan of a year ago.

Progress on heat and buildings has stalled, due in part to the failure of the Green Homes Grant. The approach to other sectors, such as transport and agriculture, remains confused and irrational, and inadequate to achieve the government’s goals. Transport is the worst performing sector, with government action continuing to increase greenhouse gas emissions rather than reduce them.

The claimed emission reductions themselves are scarcely credible, being based on technologies that do not exist at scale in the UK (e.g. on carbon capture and on hydrogen), on policies that do not yet exist (e.g. on industry regulation and on agriculture), and on assumptions about vastly increased levels of private investment that are not supported by any evidence (particularly on transport). Where substantial emission reductions could be made for wider public benefit, e.g. on retrofitting people’s homes, the proposals do not go far enough.

Overall, the Strategy lacks urgency, coherence or precision. Far from being the promised “green industrial revolution”, the Strategy seems focused on merely incremental change, such as from internal combustion engines to electric ones, from fossil-fuel boilers to low-carbon heating appliances, with continuing support for unsustainable aviation. There is no real modal shift from private to public transport or from unsustainable to sustainable farming, and no recognition that the overall demand for energy and materials needs to be reduced.

This Strategy fails to demonstrate that the UK can stay within its Sixth Carbon Budget, which is itself too loose to ensure that the UK makes its fair contribution to limiting global temperature increases to 1.5 degrees Celsius.

The Strategy takes no account of the UK’s historical responsibility for greenhouse gas emissions or for emissions embodied in imports or of the City of London’s key role in funding fossil fuels. It has nothing to say about divesting from fossil-fuel companies or about banks and pension funds divesting from those companies. It offers no forms of regulation or mandatory legislation that would be sufficient to bring about the necessary divestment.

The Strategy exudes complacency by failing to comply with Committee on Climate Change (CCC) recommendations. Ministers have apparently ignored the CCC’s 2021 report to parliament, which stated (p. 16): “credible policies for delivery currently cover only around 20% of the required reduction in emissions to meet the Sixth Carbon Budget”. They effectively postpone decisive mitigative action until after 2025.

The only amendment it suggests to the Climate Change Act 2008 is one that would include negative emissions technologies in the carbon budget: this would make the carbon budget even looser than it is already, thus reducing the need for immediate and effective action – yet another clear step backwards in the struggle to prevent catastrophic climate change.

Above all, the Strategy continues to promote alleged climate “solutions” that exist, if at all, only in the longer term (e.g. nuclear power and carbon capture and storage), while failing to act decisively in the short term – and indeed continuing to support and encourage the fossil fuel extraction and burning that is primarily responsible for causing the current global climate emergency.

Note. Researchers measure carbon dioxide (CO2) emissions in tonnes (or grams, or any other weight). Carbon dioxide makes up about three-quarters of the greenhouse gases that go into the atmosphere; most of the remainder is methane, nitrous oxide and various hydrofluorocarbons. To measure all these gases together, researchers use tonnes (or grams, or any other weight) of carbon dioxide equivalent (CO2e). The other gases have a greenhouse effect even more powerful than carbon dioxide. Different standards are used to “translate” these to carbon dioxide equivalents; the most common standard counts methane as 25 times more powerful than carbon dioxide, and nitrous oxide as 298 times more powerful. Here is one of the many guides available on line, and here is one from the European statistics agency. □ 29 November 2021.

□ Peter Somerville is Emeritus Professor of Social Policy at the University of Lincoln. He has previously written on People & Nature about the government’s Sixth Carbon Budget

□ Also recommended: “Why the oil industry’s pivot to carbon capture and storage – while it keeps on drilling – isn’t a climate change solution” by June Sekera and Neva Goodwin